The Electronic Data Capture (EDC) Systems Market has become a cornerstone of the global clinical research ecosystem, driven by the rapid digital transformation of the healthcare and life sciences sectors. As clinical trials continue to grow in complexity and scope, organizations are increasingly turning to advanced EDC solutions to streamline data collection, ensure compliance, and enhance the overall efficiency of research operations. With the expansion of decentralized clinical trials, rising demand for real-time data analytics, and continuous advancements in cloud technology, the EDC systems market is poised for remarkable growth over the coming decade.

Overview of the Electronic Data Capture (EDC) Systems Market

Electronic Data Capture (EDC) refers to a computerized system designed to collect, manage, and store data generated during clinical trials. Traditionally, data in clinical trials were recorded manually using paper case report forms (CRFs), which often led to data entry errors, delays, and higher operational costs. EDC systems have revolutionized this process by offering a digital platform that enables researchers to capture, validate, and analyze data electronically.

These systems not only reduce manual errors but also improve data integrity, compliance with regulatory standards such as FDA 21 CFR Part 11, and overall trial transparency. The EDC market encompasses a variety of software solutions tailored for pharmaceutical companies, contract research organizations (CROs), biotechnology firms, and academic research institutions.

Market Size and Growth Prospects

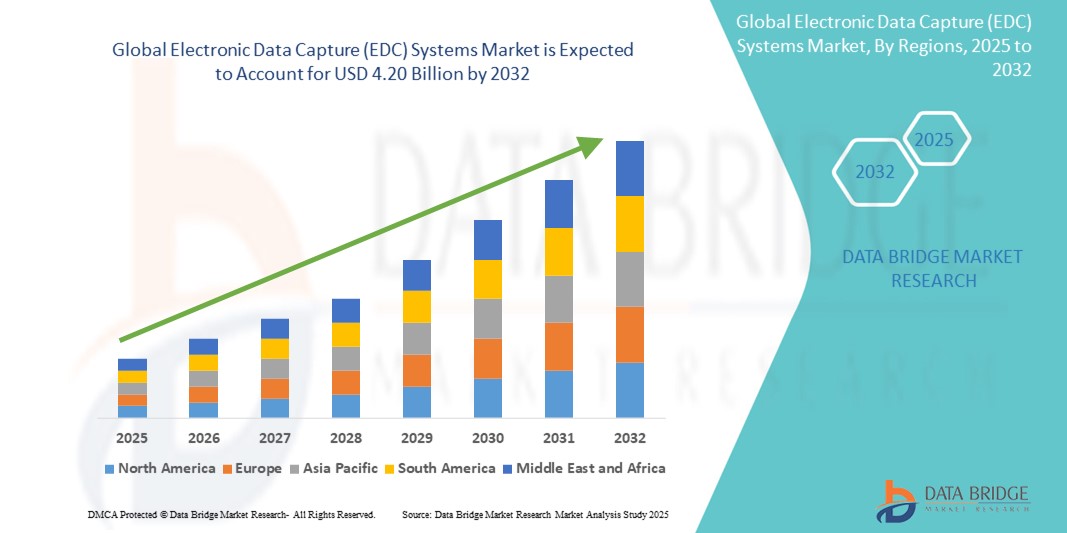

The global Electronic Data Capture Systems Market has been witnessing steady growth over the past few years. This momentum is expected to continue as more pharmaceutical companies adopt digital solutions to optimize research efficiency. Market analysts estimate that the EDC systems market will register a compound annual growth rate (CAGR) of over 10% during the forecast period (2025–2032).

This expansion is driven by increasing R&D investments, the rising number of clinical trials, and growing emphasis on patient-centric data collection approaches. Additionally, the COVID-19 pandemic accelerated the digital transformation of clinical trials, compelling organizations to adopt EDC platforms to support remote data collection and real-time monitoring.

Key Market Drivers

1. Rising Volume and Complexity of Clinical Trials

The number of clinical trials conducted globally has surged, particularly in oncology, neurology, and infectious diseases. Modern clinical trials involve multiple sites and diverse patient populations, making traditional data collection methods inefficient. EDC systems provide centralized, cloud-based platforms that facilitate faster data capture, remote access, and seamless collaboration among research teams.

2. Growing Adoption of Decentralized Clinical Trials (DCTs)

The shift toward decentralized clinical trials has been one of the most significant developments in the clinical research landscape. EDC systems play a pivotal role in enabling decentralized and hybrid trial models by integrating data from multiple sources—such as wearable devices, patient-reported outcomes (PROs), and electronic health records (EHRs). This integration allows researchers to collect real-world data efficiently and maintain high data accuracy.

3. Increasing Regulatory Compliance Requirements

Regulatory agencies, including the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA), emphasize the importance of data transparency, accuracy, and traceability in clinical research. EDC systems are designed to comply with these standards by providing features such as audit trails, secure access control, and electronic signatures. These capabilities reduce compliance risks and ensure adherence to global regulatory frameworks.

4. Advancements in Cloud and Mobile Technology

Cloud-based EDC solutions have gained prominence due to their scalability, cost efficiency, and ease of deployment. Mobile-friendly EDC platforms also enable on-site investigators and patients to input data in real time, enhancing convenience and reducing delays in data entry. The integration of artificial intelligence (AI) and machine learning (ML) further strengthens EDC systems by enabling automated data validation and predictive analytics.

Market Restraints

Despite the strong growth outlook, several challenges may hinder the widespread adoption of EDC systems. High initial implementation costs, particularly for small and mid-sized research organizations, can limit market penetration. Additionally, concerns regarding data security and interoperability between EDC systems and legacy healthcare IT infrastructures remain key obstacles. The lack of technical expertise and resistance to digital transformation in some developing regions also pose barriers to market expansion.

Segmentation Analysis

The Electronic Data Capture Systems Market can be segmented by component, delivery mode, end-user, and region.

By Component

-

Software: Represents the largest share, encompassing cloud-based and on-premise solutions for data entry, management, and reporting.

-

Services: Include system implementation, integration, training, and support. As clinical trial operations become more complex, demand for managed services continues to rise.

By Delivery Mode

-

Cloud-Based EDC Systems: Expected to dominate the market due to cost-effectiveness, real-time accessibility, and ease of integration with other eClinical solutions.

-

On-Premise Systems: Still preferred by organizations that prioritize full data control and internal security management.

By End-User

-

Pharmaceutical and Biotechnology Companies: Major contributors to market revenue, driven by increasing drug development activity.

-

Contract Research Organizations (CROs): Rapid adoption of EDC systems to enhance trial management efficiency and reduce timelines.

-

Academic Research Institutions and Hospitals: Growing use of EDC solutions for investigator-initiated and observational studies.

Regional Insights

-

North America dominates the global EDC market, supported by a strong pharmaceutical industry, regulatory mandates, and advanced digital infrastructure. The U.S. accounts for the largest share, with widespread adoption among CROs and large pharma companies.

-

Europe follows closely, driven by robust R&D activities and government initiatives promoting clinical data transparency.

-

Asia-Pacific is expected to register the fastest growth rate, propelled by the increasing number of clinical trials in countries like India, China, and Japan, along with growing investments in healthcare digitization.

-

Latin America and Middle East & Africa are emerging markets showing gradual adoption due to improvements in healthcare infrastructure and growing interest from global CROs.

Competitive Landscape

The Electronic Data Capture Systems Market is highly competitive, featuring both established players and emerging technology providers. Key companies are investing in innovation, partnerships, and AI integration to differentiate their offerings. Prominent players include:

-

Oracle Corporation

-

Medidata Solutions (Dassault Systèmes)

-

Veeva Systems Inc.

-

Data Management Services (DMS)

-

OpenClinica LLC

-

Castor EDC

-

eClinicalWorks

-

IBM Corporation

-

ClinCapture Inc.

These companies focus on expanding their product portfolios with advanced analytics, interoperability features, and mobile-friendly interfaces to address the evolving needs of clinical researchers.

Future Outlook

The future of the EDC systems market lies in integration and intelligence. As the industry shifts toward end-to-end eClinical platforms, EDC systems will increasingly integrate with complementary technologies such as clinical trial management systems (CTMS), electronic patient-reported outcomes (ePRO), and risk-based monitoring (RBM) tools.

Moreover, artificial intelligence and blockchain are expected to play transformative roles in enhancing data security, transparency, and predictive capabilities. The adoption of EDC systems will also extend beyond traditional clinical trials into real-world evidence (RWE) studies, post-market surveillance, and patient registries, broadening the market’s scope.

Conclusion

The Electronic Data Capture (EDC) Systems Market stands at the forefront of the digital revolution in clinical research. As the healthcare industry continues to prioritize data accuracy, regulatory compliance, and operational efficiency, EDC systems are becoming indispensable. With technological innovations, growing adoption of decentralized trials, and increasing global research collaborations, the EDC market is set for substantial and sustained growth.

Tags: #electronicdatacaptureedcsystems #electronicdatacaptureedcsystemspdf #listofedcsystemsclinicaltrials #electronicdatacaptureexamples #listofelectronicdatacapturesystems #edcclinicaltrialsexamples #typesofelectronicdatacapturesystems #electronicdatacapturesoftware #electronicdatacapturetools